|

Home > Business > Investment Tools > WebCab Portfolio (J2EE Edition) > Screenshots

WebCab Portfolio (J2EE Edition) Screenshots

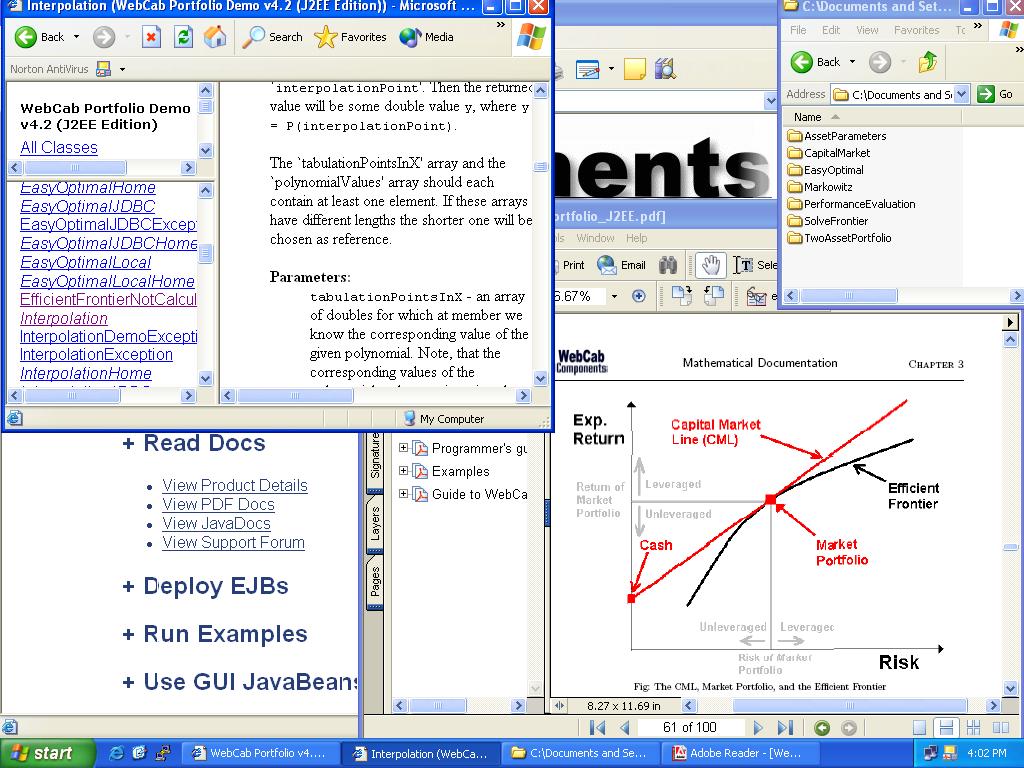

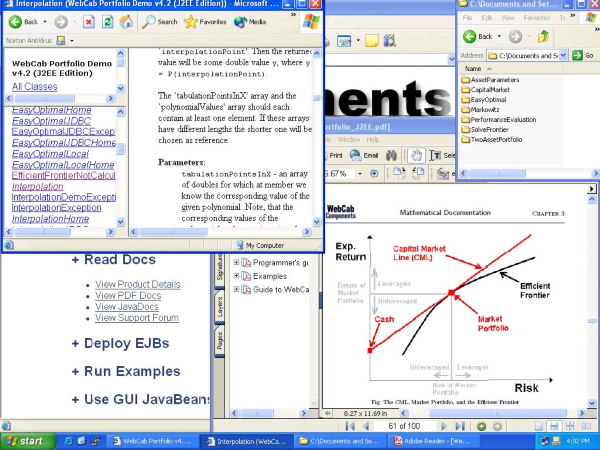

Apply the Markowitz Theory and CAPM to construct the optimal portfolio.

Apply the Markowitz Theory and CAPM to construct the optimal portfolio with/without asset weight constraints with respect to the risk, return or investors utility function. Also Performance Eval, interpolation, analysis of Efficient Frontier and CML.

Version: 4.2

System : WinOther,Win98,Win2000,WinXP,WinServer,Unix,Linux,Other,Mac OS X

Description:

Apply the Markowitz Theory and CAPM to construct the optimal portfolio with/without asset weight constraints with respect to the risk, return or investors utility function. Also Performance Eval, interpolation, analysis of Efficient Frontier and CML.

|

TAGS OF WEBCAB PORTFOLIO (J2EE EDITION)

avast antivirus mac edition ,

penjualan small business edition ,

ad-aware anniversary edition ,

threatfire antivirus free edition ,

avg free edition ,

bug doctor edition ,

pdf viewer developers edition ,

canvas professional edition ,

crm-express standard edition

|

|

|

RSS Feeds

BBS Forum

RSS Feeds

BBS Forum